A reader asked for my take on this BBC radio programme (30mins) on Q.E. I really don't know what will happen when Q.E. ends, but this is my summary of programme and thoughts on Q.E. so far.

Risks / Criticisms of Q.E.

- The new inflow of money into commercial banks from quantitative easing has encouraged banks to use this extra money through greater risk taking.

- Bond traders have benefited from making large profits out of the Bank of England by manipulating the bond market.

- Because government debt is being financed by quantitative easing, the government has less market discipline to think about reducing fiscal deficits

- Quantitative easing has been a stealth method of reducing the value of the Pound and Dollar – and therefore making UK exports cheaper. Some commentators call this currency manipulation (or currency wars).

- The increase in money supply has led to an unexpected rise in commodity prices, such as oil, leading to cost-push inflation.

- By depressing interest rates, quantitative easing has wiped out people’s return on savings

- Quantitative easing is causing inflation in the UK, and when the velocity of circulation rises, these extra bank balances will be lent – causing a possible inflationary surge.

- The scale of quantitative easing could make it impossible to sell bonds back to market and this will damage the UK’s ability to borrow in the future.

- Evidence in US, suggests even raising the possibility of tapering could cause damage to the bond market, and higher interest rates rates.

Defence of Q.E.

- There is no real evidence that there has been a surge in risky bank lending. – A more potent criticism of Q.E. is perhaps that it did so little to increase commercial bank lending.

- We need fiscal expansion not austerity. It is a very good thing if Quantitative easing has reduced the need for austerity and immediate measures to cut budget deficits.

- No currency manipulation. It is hard to accuse the UK of currency manipulation when we have a current account deficit of nearly 3% of GDP.

- Inflation has not been a macro-economic problem since 2008. The main macro-problem has been significant fall in GDP and unemployment. The Bank of England are correct to concentrate on these real problems.

- Europe inflation still too low. Inflation in the ECB is 0.8% – that is still low and creates the risk of deflationary pressures. This suggests the ECB have done too little money creation and have pursued too tight monetary policy.

- Unemployment in the Eurozone is 12%, significantly higher than the UK. UK unemployment may well be higher, if we hadn’t pursued quantitative easing.

- Future inflationary surge? It is true that if the velocity of circulation rises, there could be inflationary pressure. But, given the level of unemployment and spare capacity in the economy, the inflationary surge is hard to see.

- More on Risks vs Benefits of Q.E.

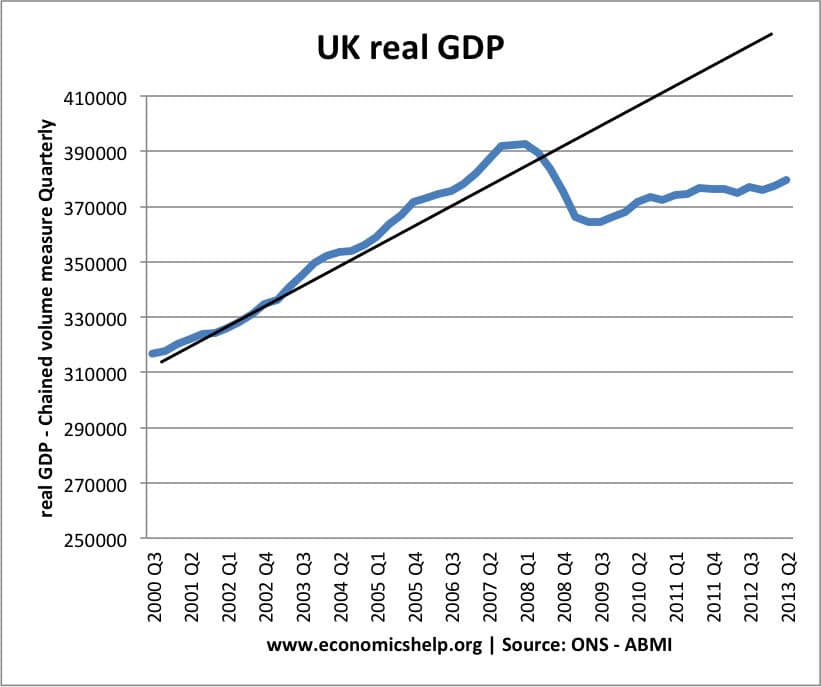

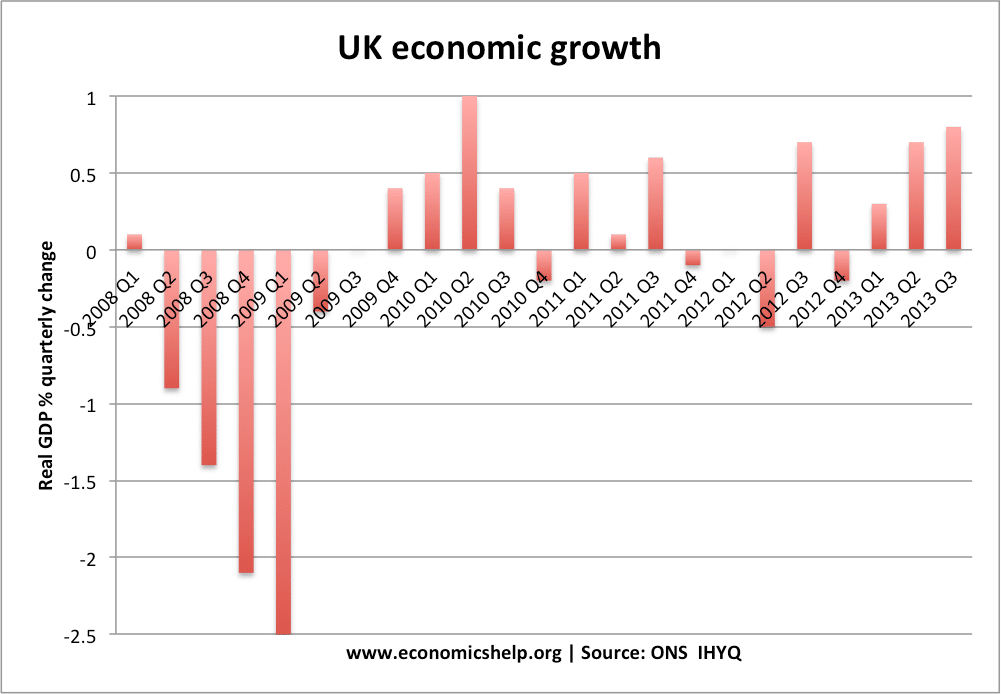

UK Recovery - weak or strong?

There are different ways of looking at the UK recovery. Firstly, we can look at the damage done to the economy since the peak in 2008.

In Q3 2013 GDP was estimated to be still

2.5% below the peak in Q1 2008. From peak to trough in 2009, the economy

shrank by 7.2%. This is an unprecedented length of economic stagnation –

compare this recession to great depression of 1930s.

Could recovery have come earlier?

There is a strong case that the signs of recovery in 2009/10 could have

been maintained with more careful policy.

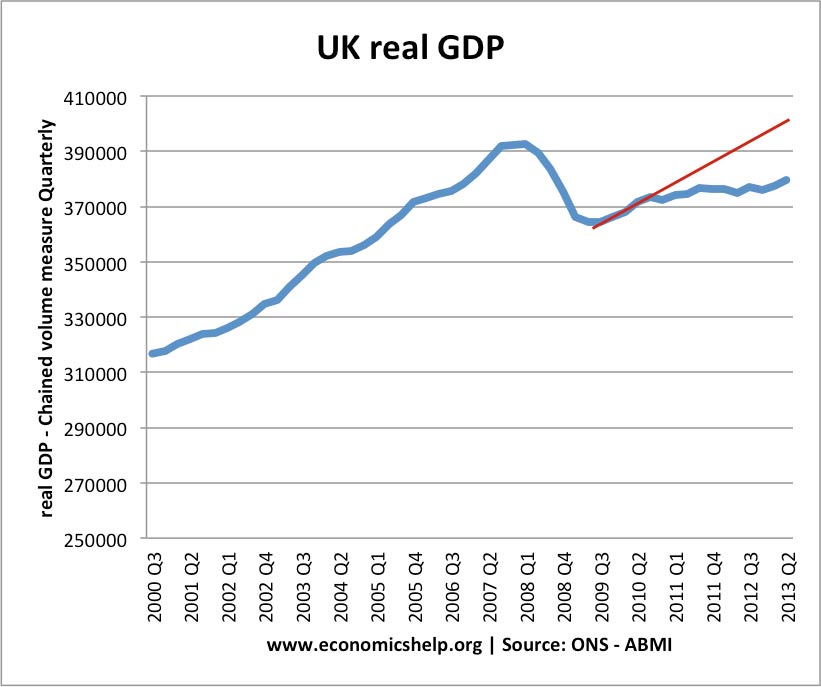

A strong bounce-back

Another way of looking at the recovery is

to concentrate on 2013. This looks much more promising, with the economy

expanding 1.8% in the first three quarters. After five years of

declining GDP, this is a great relief. The government might use this

‘strong recovery’ as vindication for their policies of austerity.

Criticism of German economic policy

Recently, the US Treasury criticised German economic policy. They argue that German’s export led growth model and anaemic pace of domestic demand is damaging to European and global growth.

“Germany’s anaemic pace of domestic

demand growth and dependence on exports have hampered rebalancing at a

time when many other euro-area countries have been under severe pressure

to curb demand and compress imports in order to promote adjustment,”

“The net result has been a deflationary bias for the euro area as well as for the world economy.” (BBC link)

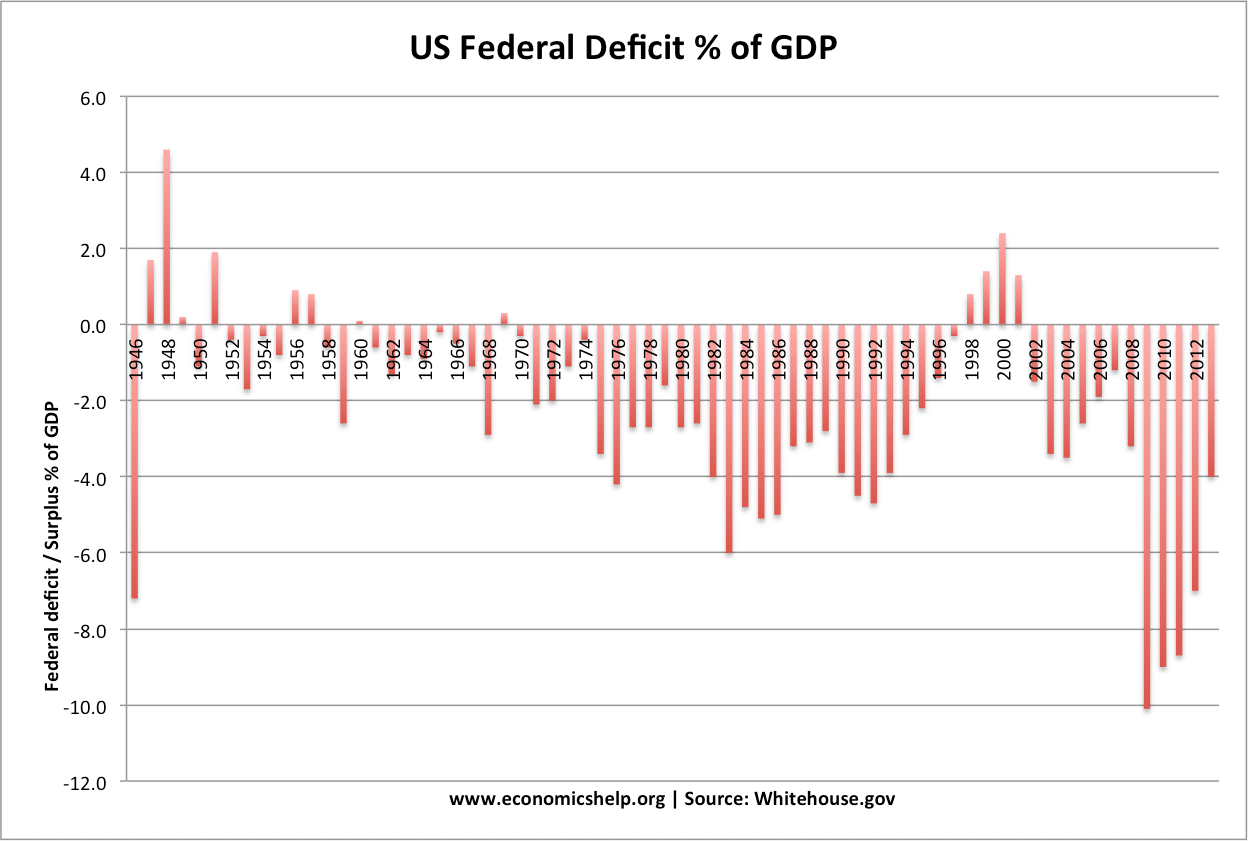

US deficit

The surprising decline of the US budget deficit.

A level

Readers Questions

- 11 questions on nature of economics and money

- The impact of the exchange rate on business

- Should we be taxing Coca-cola and other soft drinks?

- Study suggests immigrants make net contribution of (taxes - benefits) to Treasury - Impact of immigration on UK economy

- What I do when not writing economics - Cycling up hills

No comments:

Post a Comment