See part 1: Economics of the Naughties

Financial Markets need regulating.

Financial deregulation has been a disaster. Unchecked, the credit crisis shows that financial institutions can make basic mistakes in the pursuit of risky profit. Supporters of the free market have vainly tried to show the irresponsible loans of the naughties was actually due to government pressure. But, this is misleading, it was unregulated financial companies who made the vast majority of loans that had no chance of being repaid. There was a complete failure to adequately measure the level of risk involved in the buying of subprime loans. Somehow many of the NINJA mortgages (no income, no job) were rebundled, repacked and bundled as triple AAA credit rating. Western banks took these mortgages on, and it was the taxpayer who had to bailout their mistakes. Many banks pursued risky strategies of reducing liquidity ratios. There was a temptation to achieve short term profits by borrowing short to lend long. Northern Rock was once proud of it 125% mortgages. But, when the credit crisis hit, they were left unable to finance its positions. It was only when credit markets froze that they realised their business structure was flawed.

The Problem of Moral Hazard

A real problem we have is that banks acted on a premise of invulnerability. As we mentioned in this post, bankers often have an incentive to pursue risk. (problem of bank bonuses) Heads they win - tail the taxpayers lose. This is still a pressing issue - how to balance the need to ensure banking stability and prevent bank runs, without giving bankers a green light to pursue the most irresponsible strategy - knowing if they mess up someone else will clean it up.

One Tool Does Not fit

In the middle of the 2000s, it seemed that interest rates were the magic wand of the central bank to achieve any economic goal they wanted. Alas, this is not the case. Managing the economy is much more difficult that just changing interest rates. An interest rate cannot maintain strong growth, target inflation, and target asset bubbles all at the same time.

Keynesian economics

At the start of the recession, interest rates were slashed from 5% to 0%, without effect. We were in a liquidity trap where rate cuts may have no effect. In a liquidity trap, there is need for more - expansionary fiscal policy, quantitative easing. Faced with the failure of markets and the prospect of another Great Depression. The analysis of Keynes from the 1930s became very important.

Government Borrowing is necessary in a recession

One of the difficult things has been to explain, though government borrowing is bad, it would be even worse to try and reduce borrowing in the middle of a recession.

A boom is a time to reduce deficits.

Hindsight is a wonderful thing. But, at the height of the boom the decision to increase government borrowing was a painful mistake. America cut taxes and increased military spending. The UK increased spending on social security and health care. This meant both had large deficits before the recession started. This reduced room for maneouvre when the recession came.

Inflation Target can be Misleading

The central policy target of both UK and US was low inflation. With low inflation, neither governments could believe they were in the middle of an unsustainable boom. The low inflation rate, masked a boom in asset prices caused by unsustainable lending. A stable economy doesn't just need low inflation it needs stable asset prices, and sustainable bank lending.

Related

Tuesday, December 22, 2009

Monday, December 21, 2009

Economics of the Naughties

At the turn of the millennium, the landscape of economics was quite different. It was a period when major economies like the US and UK briefly had budget surpluses. It was a period of great optimism with people talking about the end of business cycle. For many analysts the world economy was living proof of the triumph of market forces, the efficient market hypothesis, and belief in the strength of unchecked capitalism. Yet, at the end of the decade, the global economy is still reeling from the biggest crisis since the Great Depression of the 1930s.

Here's a brief overview of some of the major economic events in the past decade.

The 2001 Recession

The terrorist attacks of 2001, contributed to a sharp downturn in the US economy leading to a mild recession. Faced with plummeting markets and falling output, the Federal Reserve acted quickly to cut interest rates and restore economic growth. The ease with which the Federal Reserve averted a prolonged downturn led to a round of self-congratulation amongst leading policy makers. As Paul Krugman noted 1997, it really did seem that:

It was also a period of financial deregulation, and financial innovation. Rising house prices encouraged a rash of new mortgage types. Never had it been so easy to get a mortgage. The combination of low interest rates and financial deregulation encouraged a new generation of homeowners to take out mortgages that previously would have been unthinkable. Based on a great sense of optimism of (seemingly) permanently rising house prices, banks seemed willing to lend a mortgage to just about anyone who could sign on a dotted line.

In the middle of a boom, the US cut income taxes and the UK increased government spending. Both of which caused a structural budget deficit. This worried few people at a time of prosperity, but was to become much more significant later.

Boom and Bust

With low inflation, low unemployment and strong growth. It appeared policy makers had achieved the holy grail of economic stability and constant growth. Talk of the end of the business cycle was common.

But, this stability masked an asset boom and a rise in unsustainable subprime lending, that nobody seemed to be aware about. At the start of 2006, few if any could have predicted how fragile the global financial system was. Healthy profits masked a much different story.

After keeping interest rates too low for too long, in 2005-06, the Federal Reserve finally began to increase interest rates. Nothing spectacular, interest rates were increased to 5%. But, even this modest rise in interest rates sparked one of the most spectacular wave of loan defaults the world economy has ever seen. It was only after a modest rise in interest rates that people started to realise how absurd many mortgage deals had been made.

After rising inexorably and against many optimistic forecasts (see: Books they wish they hadn't written ), US House prices started to fall and nervous banks started to realise alot of their sub-prime mortgages had all the foundations of a sand castle, based on the assumption the sea would always keep retreating.

In other times, this wave of mortgage defaults may have stayed in America. But, thanks to financial deregulation and a collective amnesia in analysing risk, the financial community had very nicely spread these toxic subprime loans all around the global financial system, rebundling them into seemingly anonymous Collateral Debt Obligations CDOs. If you don't understand what a CDO is, it seems many professional bankers didn't really know what they were buying either.

The result was that suddenly the liquidity evaporated from the global banking system. Everyone was hurrying to try and improve their balance sheets and recall toxic loans. But, it was too late, no-one wanted to lend to each other anymore. The cleverest and riskiest banking strategies now appeared for what they were - a recipe for self-bankruptcy. It all seemed like a bad joke, except, it was a very expensive joke with the taxpayer paying - see humorous look at sumprime crisis)

For more details see step by step Credit Crunch explained -

In the summer and autumn of 2008, it appeared no financial institution was safe. Just when you thought it could get no worse, another huge financial company announced they were on the verge of bankruptcy. Northern Rock, Bradford & Bingley, JP Mogan, Citigroup (to list but a small number who received government bailouts). Mostly, the taxpayer rode to the rescue and bailed out the banks with mind blowing sums. But, for whatever reason, when it came to Lehman Brothers, the American authorities decided to say "sorry, but, no". It was perhaps a brave and courageous decision. But, it was a decision they were to quickly regret. Financial markets and consumers panicked - the great assumption that no bank could possibly fail was suddenly exposed as a myth. Now, no bank now was safe. The only thing to do well was gold and mattresses as people sought to hoard their wealth in gold or cash under the bed.

The crisis precipitated the biggest fall in GDP since the great depression. In fact the start of the 2008 recession was just as severe as the Great Depression. With collapsing house prices, banks on the verge of bankruptcy, and confidence hammered, there was a real possibility of another depression.

To be fair after making so many mistakes in allowing the bubble and credit crunch, the response of governments to the crisis was reasonable. At least some of the mistakes of the Great Depression had been learnt. Though it is a bitter pill to swallow, governments prevented more bank collapses with bailouts. Interest rates were slashed, expansionary fiscal policy was pursued and even the unorthodox monetary policy of quantitative easing was pursued to avoid the great threat of deflation.

The most pessimistic forecasts of another depression have been averted. But, that doesn't mean all is well. Far from it. Banks still nurse fragile balance sheets, economies are being propped up with unprecedented government intervention. Public debt has ballooned creating real threats of government default in various western economies. The recovery will be very difficult. Trying to balancing record debt against the need to maintain growth.

It was also a decade where the problems of global warming became increasingly apparent. But, a problem the global community seem unable or unwilling to tackle. If the scientific forecasts for global warming prove correct, the credit crisis could seem a minor problem compared to the devastation caused by rising sea levels and weather crisis.

Tomorrow:

Lessons from the Economics of the Naughties.

Here's a brief overview of some of the major economic events in the past decade.

The 2001 Recession

The terrorist attacks of 2001, contributed to a sharp downturn in the US economy leading to a mild recession. Faced with plummeting markets and falling output, the Federal Reserve acted quickly to cut interest rates and restore economic growth. The ease with which the Federal Reserve averted a prolonged downturn led to a round of self-congratulation amongst leading policy makers. As Paul Krugman noted 1997, it really did seem that:

“If you want a simple model for predicting the unemployment rate in the United States over the next few years, here it is: it will be what [Alan] Greenspan wants it to be, plus or minus a random error reflecting the fact that he is not quite God.” (When Greenspan was nearly God)

It was also a period of financial deregulation, and financial innovation. Rising house prices encouraged a rash of new mortgage types. Never had it been so easy to get a mortgage. The combination of low interest rates and financial deregulation encouraged a new generation of homeowners to take out mortgages that previously would have been unthinkable. Based on a great sense of optimism of (seemingly) permanently rising house prices, banks seemed willing to lend a mortgage to just about anyone who could sign on a dotted line.

In the middle of a boom, the US cut income taxes and the UK increased government spending. Both of which caused a structural budget deficit. This worried few people at a time of prosperity, but was to become much more significant later.

Boom and Bust

With low inflation, low unemployment and strong growth. It appeared policy makers had achieved the holy grail of economic stability and constant growth. Talk of the end of the business cycle was common.

But, this stability masked an asset boom and a rise in unsustainable subprime lending, that nobody seemed to be aware about. At the start of 2006, few if any could have predicted how fragile the global financial system was. Healthy profits masked a much different story.

After keeping interest rates too low for too long, in 2005-06, the Federal Reserve finally began to increase interest rates. Nothing spectacular, interest rates were increased to 5%. But, even this modest rise in interest rates sparked one of the most spectacular wave of loan defaults the world economy has ever seen. It was only after a modest rise in interest rates that people started to realise how absurd many mortgage deals had been made.

After rising inexorably and against many optimistic forecasts (see: Books they wish they hadn't written ), US House prices started to fall and nervous banks started to realise alot of their sub-prime mortgages had all the foundations of a sand castle, based on the assumption the sea would always keep retreating.

In other times, this wave of mortgage defaults may have stayed in America. But, thanks to financial deregulation and a collective amnesia in analysing risk, the financial community had very nicely spread these toxic subprime loans all around the global financial system, rebundling them into seemingly anonymous Collateral Debt Obligations CDOs. If you don't understand what a CDO is, it seems many professional bankers didn't really know what they were buying either.

The result was that suddenly the liquidity evaporated from the global banking system. Everyone was hurrying to try and improve their balance sheets and recall toxic loans. But, it was too late, no-one wanted to lend to each other anymore. The cleverest and riskiest banking strategies now appeared for what they were - a recipe for self-bankruptcy. It all seemed like a bad joke, except, it was a very expensive joke with the taxpayer paying - see humorous look at sumprime crisis)

For more details see step by step Credit Crunch explained -

In the summer and autumn of 2008, it appeared no financial institution was safe. Just when you thought it could get no worse, another huge financial company announced they were on the verge of bankruptcy. Northern Rock, Bradford & Bingley, JP Mogan, Citigroup (to list but a small number who received government bailouts). Mostly, the taxpayer rode to the rescue and bailed out the banks with mind blowing sums. But, for whatever reason, when it came to Lehman Brothers, the American authorities decided to say "sorry, but, no". It was perhaps a brave and courageous decision. But, it was a decision they were to quickly regret. Financial markets and consumers panicked - the great assumption that no bank could possibly fail was suddenly exposed as a myth. Now, no bank now was safe. The only thing to do well was gold and mattresses as people sought to hoard their wealth in gold or cash under the bed.

The crisis precipitated the biggest fall in GDP since the great depression. In fact the start of the 2008 recession was just as severe as the Great Depression. With collapsing house prices, banks on the verge of bankruptcy, and confidence hammered, there was a real possibility of another depression.

To be fair after making so many mistakes in allowing the bubble and credit crunch, the response of governments to the crisis was reasonable. At least some of the mistakes of the Great Depression had been learnt. Though it is a bitter pill to swallow, governments prevented more bank collapses with bailouts. Interest rates were slashed, expansionary fiscal policy was pursued and even the unorthodox monetary policy of quantitative easing was pursued to avoid the great threat of deflation.

The most pessimistic forecasts of another depression have been averted. But, that doesn't mean all is well. Far from it. Banks still nurse fragile balance sheets, economies are being propped up with unprecedented government intervention. Public debt has ballooned creating real threats of government default in various western economies. The recovery will be very difficult. Trying to balancing record debt against the need to maintain growth.

It was also a decade where the problems of global warming became increasingly apparent. But, a problem the global community seem unable or unwilling to tackle. If the scientific forecasts for global warming prove correct, the credit crisis could seem a minor problem compared to the devastation caused by rising sea levels and weather crisis.

Tomorrow:

Lessons from the Economics of the Naughties.

Monday, December 7, 2009

US Economy in 2010

After the deepest recession since the Great Depression, there is understandably considerable relief at the first signs of growth in the US. Recent job figures also suggest the economy has turned. However, some commentators worry that these first greenshoots could lead to a complacent feeling and that the US economy still faces many weakness in 2010.

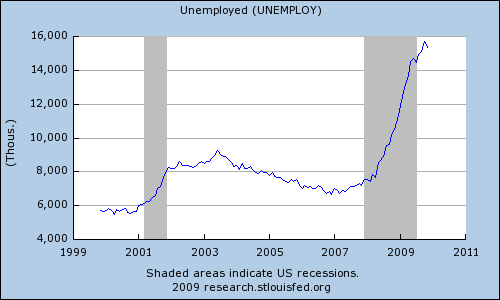

This graphs shows the extent of the decline in economic output. The recession of 2009 easily dwarves the modest decline of 2001. The red line indicates the potential rate of economic growth. This shows how much spare capacity will exist in the US economy in 2010, this will make it difficult to tackle the unemployment problem. The sharp rise in unemployment is perhaps the biggest problem facing the US economy. Like the UK, the rise in unemployment has been muted by a fall in working hours and increase in temporary employment. The bad news is that the forecast for unemployment in 2010 and 2011 is for a continued period of high unemployment.

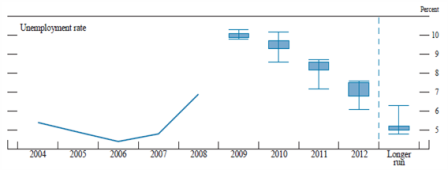

The sharp rise in unemployment is perhaps the biggest problem facing the US economy. Like the UK, the rise in unemployment has been muted by a fall in working hours and increase in temporary employment. The bad news is that the forecast for unemployment in 2010 and 2011 is for a continued period of high unemployment. Unemployment rates in 2010 and 2011 - source: P.Krugman

Unemployment rates in 2010 and 2011 - source: P.Krugman

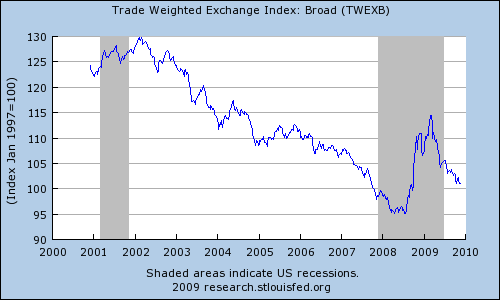

The Dollar in 2010

Many people might be a little surprise at how much the dollar rallied from the summer of 2008. But, this year, the dollar has regained its downward momentum, and it is hard to see a reversal in the dollar fortunes given state of economy.

Many people might be a little surprise at how much the dollar rallied from the summer of 2008. But, this year, the dollar has regained its downward momentum, and it is hard to see a reversal in the dollar fortunes given state of economy.

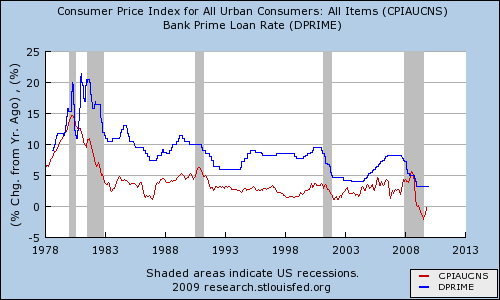

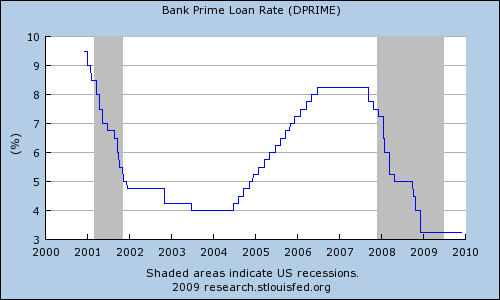

There are some who apparently worry about inflation prospects in the US. But, I still feel the US has more to fear from inflation than deflation. Inflation is likely to remain low during 2010 because of the spare capacity and lack of wage pressures. As a consequence, interest rates are likely to remain low throughout 2010.

Related

Image Sources: St Louis Fed

Economic Growth and Spare Capacity

This graphs shows the extent of the decline in economic output. The recession of 2009 easily dwarves the modest decline of 2001. The red line indicates the potential rate of economic growth. This shows how much spare capacity will exist in the US economy in 2010, this will make it difficult to tackle the unemployment problem.

Unemployment in US

The sharp rise in unemployment is perhaps the biggest problem facing the US economy. Like the UK, the rise in unemployment has been muted by a fall in working hours and increase in temporary employment. The bad news is that the forecast for unemployment in 2010 and 2011 is for a continued period of high unemployment.

The sharp rise in unemployment is perhaps the biggest problem facing the US economy. Like the UK, the rise in unemployment has been muted by a fall in working hours and increase in temporary employment. The bad news is that the forecast for unemployment in 2010 and 2011 is for a continued period of high unemployment.Forecast for US Unemployment

Unemployment rates in 2010 and 2011 - source: P.Krugman

Unemployment rates in 2010 and 2011 - source: P.KrugmanThe Problem with US Banking Sector

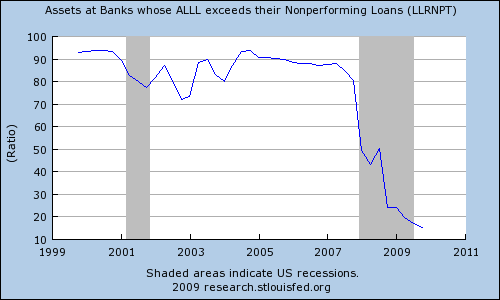

As we mentioned in a recent post - Worries over future home foreclosures - the US banking sector still faces more potential losses from home repossessions. This graph shows how much banks have been affected by the housing market crash and credit crunch. It will take a long time for banks to recover balance sheets and ability to lend like before the crash.Assets of US Banks

Budget Deficit

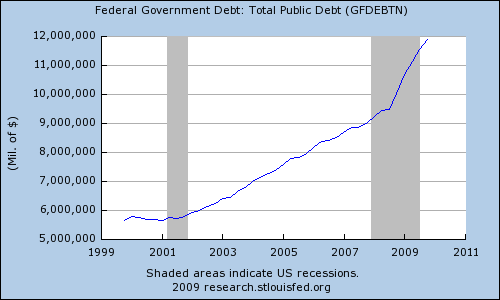

The US budget deficit continues its remorseless rise. Now over $12 trillion, it continues to rise as a % of GDP. It has also become an important political issue. With more voters apparantely concerned about the deficit than unemployment. The debt is a long term problem, but, efforts to reduce it in the short term could dampen the economic recovery and push the economy back into recession.

The Dollar in 2010

Many people might be a little surprise at how much the dollar rallied from the summer of 2008. But, this year, the dollar has regained its downward momentum, and it is hard to see a reversal in the dollar fortunes given state of economy.

Many people might be a little surprise at how much the dollar rallied from the summer of 2008. But, this year, the dollar has regained its downward momentum, and it is hard to see a reversal in the dollar fortunes given state of economy.Inflation and Interest Rates

There are some who apparently worry about inflation prospects in the US. But, I still feel the US has more to fear from inflation than deflation. Inflation is likely to remain low during 2010 because of the spare capacity and lack of wage pressures. As a consequence, interest rates are likely to remain low throughout 2010.

Related

Image Sources: St Louis Fed

Subscribe to:

Comments (Atom)