Many have been told dire stories of German hyperinflation in the 1920s causing economic upheaval, the rise of Hitler e.t.c. Because of events such as this and in Zimbabwe, there is a strong assumption that inflation is always and everywhere a serious economic problem.

Low inflation (of around 2% ) is indeed the primary economic target of all major economies. Everyone assumes inflation is bad, but, how really damaging is it if inflation rises above the inflation target?

Let us assume that inflation was to rise above 2% closer to 6 or 7% what would be the economic consequences?

Potential Costs of Inflation

Inflation reduces value of savings. High inflation reduces the value of money. Therefore people who keep cash under the bed will see their savings decline. But, who actually keeps money under the bed? If interest rates are higher than inflation then the real value of money will be maintained. Inflation of 7% and interest rates of 9%, is much better than the current situation of inflation 2.9% and interest rates of 0.5%. (which is a negative real interest rate). It is not the inflation rate that determines real value of savings but the real interest rate.

Inflation makes people worse off. Higher prices increase the cost of living. Again the key issue is whether nominal wages keep up with rising price level. As long as real wages remain positive people will not be worse off. All state benefits are index linked meaning that higher inflation will lead to bigger rises in benefits.

International competitiveness. A higher UK inflation rate causes UK goods to become uncompetitive. However, the inflation will also cause a depreciation in the value of pound restoring the competitiveness of exports.

Confusion and Uncertainty It is said high inflation rates create greater uncertainty and confusion leading to lower levels of investment. Alot depends on whether the inflation is anticipated or unanticipated. If inflation is anticipated the impact on uncertainty is much less.

Menu costs. Higher inflation rates mean firms will have to readjust prices more frequently. But, with modern technology it is easier to do.

The Spiral Effect. The big fear of inflation is that a moderate rise in inflation rates causes inflation to inexorably spiral upwards. If we allow inflation to rise a little, before we know it we are facing a real problem with inflation in 3 digits. In practise it is hard to control inflation once it starts to get out of hand. Therefore, its best to keep it low

Conclusion.

Targeting low inflation does make sense. By targeting low inflation we can provide a framework for sustainable and stable economic growth. It helps avoid boom and bust cycles which are very damaging.

However, maybe some Central Banks (in particular the ECB) could loosen up a little and not feel so guilty if inflation slightly overshoots the target. Many years ago, Norman Lamont told us 'unemployment is a price well worth paying for lower inflation' but, maybe this assumption is misplaced and not true. Whilst inflation does have costs, there are potentially much bigger costs of dogmatically targeting low inflation, especially in the current climate.

Also another lesson of this recession is that targeting low inflation is insufficient to maintain macroeconomic stability. The low inflation of the early 2000s seems to have given us a false impression of economic stability.

More on

Wednesday, May 20, 2009

Wednesday, May 13, 2009

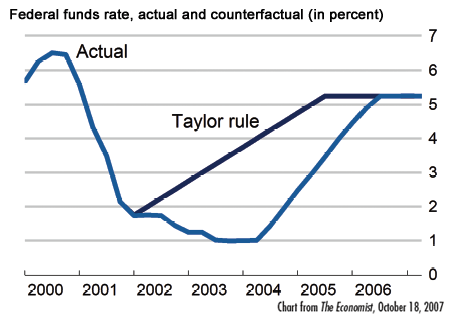

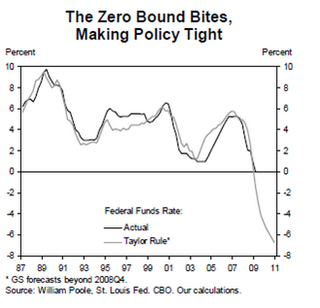

Taylor Rule and Interest Rates

The Taylor rule is a formula for setting interest rates depending on changes in the inflation rate and economic growth.

A simplified formula is: r = p + 0.5y + 0.5 (p - 2) + 2 (after Tobin, 1998)

Example of Taylor Rule:

The interesting thing is what the Taylor rule says about current interest rates. Since GDP in US has collapsed by - 4% (when growth trend is about 2%) it means that GDP is much lower than potential. Paul Krugman estimated that using the Taylor rule, the US should give a nominal interest rate of -7%. This indicates why the Federal Reserve are having to resort to quantitative easing. They can't cut interest rates below 0%, so they need to resort to unorthodox measures to boost the economy.

A simplified formula is: r = p + 0.5y + 0.5 (p - 2) + 2 (after Tobin, 1998)

- r = the short term interest rate in percentage terms per annum.

- p = the rate of inflation over the previous four quarters.

- y = the difference between real GDP from potential output.

- This assumes that target inflation is 2% and equilibrium real interest rate is 2%

Example of Taylor Rule:

- If inflation were to rise by 1%, the Taylor response would be to raise the interest rate by about 1.5%

- If GDP falls by 1% relative long run trend rate, then the Taylor response is to cut the interest rate by about 0.5%

- Basically, higher growth and inflationary pressures require higher interest rates to reduce economic activity. Lower growth and a fall in inflation require lower interest rates to boost spending.

Interest Rates Too Low in US Using Taylor Rule

The interesting thing is what the Taylor rule says about current interest rates. Since GDP in US has collapsed by - 4% (when growth trend is about 2%) it means that GDP is much lower than potential. Paul Krugman estimated that using the Taylor rule, the US should give a nominal interest rate of -7%. This indicates why the Federal Reserve are having to resort to quantitative easing. They can't cut interest rates below 0%, so they need to resort to unorthodox measures to boost the economy.

Taylor Rule and Suggested Interest Rate for US

- Interest rates explained

- source of graphs - Urbanomics Taylor Rule

- Taylor Rule - Bized

Tuesday, May 12, 2009

Deflation in Japan

Whilst there is still much debate about the likelyhood of deflation in the UK and US (see: inflation vs deflation) It is worth examining the impact of deflation in Japan. Japan has been experiencing deflation on and off since the 1990s and yesterday saw unwelcome statistics that showed a return of deflation to Japan (Official inflation rate -0.3%).

At first glance, falling prices appears to be a boon to consumers as goods and services become cheaper. But, combined with falling incomes and rising unemployment it creates a toxic mix of economic stagnation.

Paradox of Thrift. With the threat of unemployment, consumers sought to save and reduce their spending. The incentive to save is increased by falling prices. Falling prices means goods are cheaper in the future therefore people kept delaying purchases, espeically of big ticket items. The combined rise in savings reduces consumer spending. (the Japanese saving ratio did fall in this period, but, this was due to other factors such as an ageing population)

Rising Debt Burden. Deflation increases the real burden of debt. This caused problems for firms and consumers with large debts, discouraging investment and spending. Deflation in the UK and US would be even more damaging because consumers are more exposed to debt.

Fiscal Policy. Japan did try various measures of fiscal expansion such as government spending schemes. But, these were often inadequate. Unfortunately, Japan's economic crisis coincided with concerns over an ageing population and the impact on the government finances. Worried over the rising debt burden, the Government increased taxes in 1997 and promptly caused another recession. The recession led to further rises in government debt and Japanese debt now stands at close to 195% of GDP.

Difficulty in Creating Inflation.

We have got so used to worrying about inflation, it seems hard to believe that to create moderate inflation can actually be quite difficult. The Japanese Central Bank did introduce a limited form of quantitative easing, increasing the money supply by upto 12% a year but it struggled to gain normal inflationary pressures.

The recent economic recovery of Japan 05-07 was mainly export based. Thus when the global economy slowed down, Japanese GDP collapsed again leading to a further bout of deflation.

It seems deflation is an ill that persistently dogs the Japanese economy.

Deflation in Japan at BBC

At first glance, falling prices appears to be a boon to consumers as goods and services become cheaper. But, combined with falling incomes and rising unemployment it creates a toxic mix of economic stagnation.

Problems of Deflation

Price Wars. To attract consumers, firms began price cuts that became increasingly aggressive, but, the price wars did little to boost overall spending, it only led to smaller profit margins and caused many firms to go under. The fall in output caused unemployment in Japan to rise from 2% to 5%. 5% may still seem low, but, this official figure ignored a lot of disguised unemployment such as early retirement or temporary work.Paradox of Thrift. With the threat of unemployment, consumers sought to save and reduce their spending. The incentive to save is increased by falling prices. Falling prices means goods are cheaper in the future therefore people kept delaying purchases, espeically of big ticket items. The combined rise in savings reduces consumer spending. (the Japanese saving ratio did fall in this period, but, this was due to other factors such as an ageing population)

Rising Debt Burden. Deflation increases the real burden of debt. This caused problems for firms and consumers with large debts, discouraging investment and spending. Deflation in the UK and US would be even more damaging because consumers are more exposed to debt.

Difficulties in Dealing With Deflation

Zero Interest Rates. Even though Japan cut interest rates to 0%, deflation means the real interest rate remained high.Fiscal Policy. Japan did try various measures of fiscal expansion such as government spending schemes. But, these were often inadequate. Unfortunately, Japan's economic crisis coincided with concerns over an ageing population and the impact on the government finances. Worried over the rising debt burden, the Government increased taxes in 1997 and promptly caused another recession. The recession led to further rises in government debt and Japanese debt now stands at close to 195% of GDP.

Difficulty in Creating Inflation.

We have got so used to worrying about inflation, it seems hard to believe that to create moderate inflation can actually be quite difficult. The Japanese Central Bank did introduce a limited form of quantitative easing, increasing the money supply by upto 12% a year but it struggled to gain normal inflationary pressures.

The recent economic recovery of Japan 05-07 was mainly export based. Thus when the global economy slowed down, Japanese GDP collapsed again leading to a further bout of deflation.

It seems deflation is an ill that persistently dogs the Japanese economy.

Deflation in Japan at BBC

Subscribe to:

Comments (Atom)