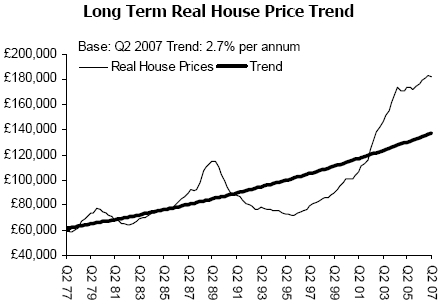

If you look at a graph of UK or American house prices - It tends to remind you of one thing - A Rollercoaster. (BTW: since end of graph, UK house prices have fallen £20,000)

Why are House prices so Volatile? Why don't house prices increase at a constant rate, or even remain close to the inflation rate.

On first glance, you might expect house prices to be steady:

- Houses are difficult to buy and sell. There are both financial costs and costs in terms of time. It's not like a stock commodity which can easily be traded.

- The majority of people who buy, do it to live in - not as a speculative investment.

Interest rates.

The last boom in house prices in the UK, was burst by a rapid increase in interest rates. If interest rates doubled from 6% to 12% alot homeowners suddenly start defaulting; it is a major disincentive to buy. Interest rates are used to control inflation and the economic cycle - not to stabilise house prices.

In the US, many housing problems were exacerbated when the Federal reserve increased rates from 2% to 4% in 2006. 4% interest rates are still relatively low, but, many had borrowed up to the hilt. This small rise in interest rates stretched their affordability.

Time Delays in Building House

When house prices are rising, builders want to increase supply. However, from planning to completion can take up to 2 years. Therefore, if builders start building at peak of boom, when prices are falling, new houses are still coming onto the market. Therefore, the increase in supply, magnifies the falling prices (particularly a problem in the US at the moment). At the start of the boom, an inelastic supply squeezes prices upwards, even with relatively moderate demand. (this is the case in the UK)

Confidence Factor

When prices are falling, people want to delay their purchase - after all it could save you tens of thousands of dollars. Therefore, falling house prices deter buyers, causing even lower prices. This is exacerbated by media headlines which highlight the 'housing crisis'

When prices are rising, the opposite happens. People see it as an opportunity to make equity gains or consolidate debt. It becomes easy for people to slip into notion that 'house prices always rise' Housing has generally been seen as the safest investment you can make - I mean it's not like buying some obscure dot com firm.

Mortgage Industry is Cyclical.

When prices are rising, mortgage firms become more willing to lend 100% mortgages. Homeowners need less deposit, because the hope is for rising house prices to effectively create the deposit. When prices are falling, the need for a deposit rises to insure mortgage firms against negative equity. This is the reason why mortgages are often more diffficult to secure during falling prices.

- Of course, during the present credit crunch the cyclical nature of the mortgage industry has reached unprecedented levels.

What determines house prices?

Overvalued housing markets

How bad are falling house prices?

More reasons to explain boom and busts in House prices

No comments:

Post a Comment